Table of Content

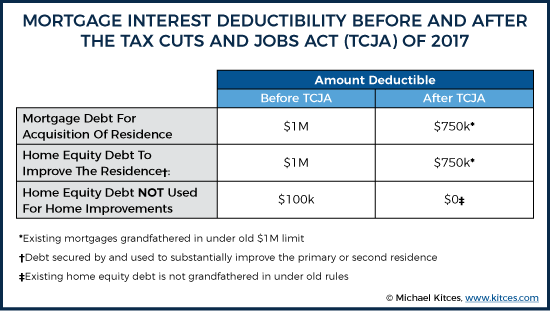

Homeowners who bought before then can still deduct the interest on mortgage debt of up to $1 million. The IRS this week clarified a provision of the Tax Cuts and Job Acts that eliminates the deduction for interest paid on home equity loans and lines of credit. You do not need to report loan proceeds as income, and you cannot deduct interest payments on those loans. However, the IRS makes an exception for personal loans that are secured by a residence, as is the case with mortgages, home equity loans, and HELOCs. You can deduct the interest on up to $750,000 in home loan debts if the loans were made after Dec. 15, 2017. If your total mortgage debt is higher than that, then you wont be able to deduct all of the combined interest paid.

Also included in this bunch are expenses related to investment fees, legal fees, home office use and alimony for divorces finalized after December 31, 2018. These deductions will be reinstated in 2026 unless Congress votes to extend the current rule. That means it will be a lot tougher to qualify to itemize deductions. If your mortgage existed on Dec. 14, 2017, you’re grandfathered in on the $1 million maximum.

How We Make Money

Highest rate is applicable to taxable income above $500,000 for single taxpayers and head of household, and $600,000 for married taxpayers filing jointly. So, many taxpayers tapped into their home equity to pay for, say, vacations, college tuition, vehicle purchases and living expenses. And they counted on deducting interest on those loans each tax year. The new rules for deducting interest on home equity loans will put a wrench in those plans, starting in 2018. The good news is not all these changes will apply this upcoming year. On December 2017, President Donald Trump signed the new tax reform law called Tax Cuts and Jobs Act.

Note the limitation is per taxpayer which increases the limitation for single co-owners / registered domestic partners. Generally, you have a reasonable basis if your chances of withstanding an IRS challenge are greater than 50%. Reliance on a competent tax advisor greatly improves your odds of obtaining penalty relief. Other possible grounds for relief include computational errors and reliance on an inaccurate W-2, 1099 or other information statement. Tax-filing inaccuracy.These penalties may be imposed, for example, if the IRS finds that your return was prepared negligently or that there’s a substantial understatement of tax.

Is There A Best Time Of Day For Therapy? Here's What Therapists Say.

It is applicable only when the mortgage is not higher than the refinanced debt. Homeowners cannot deduct the interest paid on a home equity loan or home equity line of credit if they used the debt to increase the value of the home. Say that in January 2018, a taxpayer took out a $500,000 mortgage to buy a home valued at $800,000. Then, the next month, the taxpayer took out a $250,000 home equity loan to build an addition on the home. Before, taxpayers could include state and local property taxes as itemized deductions.

The I.R.S. also noted that the new law sets a lower dollar limit on mortgages over all that qualify for the interest deduction. Beginning this year, taxpayers may deduct interest on just $750,000 in home loans. The limit applies to the combined total of loans used to buy, build or improve the taxpayer’s main home and second home. You can deduct the interest on up to $750,000 in home loan debts, if the loans were made after Dec. 15, 2017. If your total mortgage debt is higher than that, you won’t be able to deduct all of the combined interest paid. The $1 million cap applies for mortgages obtained before that date.

IRS Clarifies Home Equity Loan Tax Deductions Under New Law

For alternative minimum tax purposes, however, you could deduct the interest on these amounts only if the home equity loan proceeds were used to buy or improve your first or second residence. There are limits on the amount of home equity loan and lines of credit interest that can be deducted because the new tax law caps the total amount of home-related interest that can be written off. Interest on mortgage debt up to $750,000 can be deducted on homes purchased after Dec. 15, 2017.

However, if you use the proceeds of the loan for what the IRS deems to be "substantial improvements" to your home, and meet other criteria, home equity loan interest may still be deductible to an extent. Under the new law the interest paid on home equity loans will no longer be tax-deductible. However interest on a HELOC loan that is obtained to acquire, build or substantially improve the residence will remain deductible. Though the miscellaneous deductions outlined above have been suspended through 2025 for regular employees, self-employed workers can still write-off qualifying work-related expenses. Deductions such as self-employment taxes, insurance premiums and yes ― a home office ― can be claimed using the Schedule C form.

Interest on Home Equity Loans Is Still Deductible, but With a Big Caveat

You should receive IRS Form 1098 from your lender with details about the interest you've paid on your home equity loan. Of Schedule A (Form 1040.) Any non-tax deductible interest paid on a home equity loan needs to be reported on line 8b. Speaking with a tax preparer who is familiar with the details of your home equity loan can help you avoid any problems when taking the deduction. The private mortgage insurance deductionwas re-upped for tax year 2017. Ditto the residential energy tax credits for installing things like energy-efficient windows and doors, water heaters, furnaces, and insulation. The student loan deduction— up to $2,500 if you’re repaying — stays put, and you don’t have to itemize to take it.

According to the IRS, interest on home equity loans or home equity lines of credit is not tax deductible if the borrowed amount is not used to buy, build, or substantially improve the home against which the money was borrowed. To get more than your standard deduction, you might need a sizable loan or other expenses to help . If you are on the fence about a property remodel, then borrowing against your home just to take advantage of deducting the interest is probably not your best choice. Taking out a home equity line of credit may still be worth it even if the interest is not deductible to you, depending on how you plan to use the money. If youre interested in consolidating credit card debt, for example, and if you can get a much lower rate with a HELOC, then you could save money this way. Of course, this strategy assumes that youll pay the HELOC down as quickly as possible to minimize interest charges and that you wont run up new debt on the cards that youve paid off.

You'll start receiving the latest news, benefits, events, and programs related to AARP's mission to empower people to choose how they live as they age. We know you have many options when it comes to accounting firms in St. Paul or the Twin Cities area, and we know we’re not the right fit for everyone—but when you’re ready to start a conversation, we’ll be ready to listen. The Balance uses only high-quality sources, including peer-reviewed studies, to support the facts within our articles. Read our editorial process to learn more about how we fact-check and keep our content accurate, reliable, and trustworthy. Ebony Howard is a certified public accountant and a QuickBooks ProAdvisor tax expert. She has been in the accounting, audit, and tax profession for more than 13 years, working with individuals and a variety of companies in the health care, banking, and accounting industries.

The interest on home equity loans cannot be deducted for tax purposes if the proceeds were not used to buy, build or substantially improve your home. You can deduct interest on a home equity line of credit , but only if you use the funds for home improvements. The introduction of the Tax Cuts and Jobs Act eliminated deductions on interest if you use the funds for anything else, such as to consolidate debt.

It might even provide some tax benefits since the interest you pay is sometimes deductible. But if you use the money to pay off credit card debt or student loans — or take a vacation — the interest is no longer deductible. But the Internal Revenue Service, saying it was responding to “many questions received from taxpayers and tax professionals,” recently issued an advisory. According to the advisory, the new tax law suspends the deduction for home equity interest from 2018 to 2026 — unless the loan is used to “buy, build or substantially improve” the home that secures the loan. Under prior tax law, a taxpayer could deduct “qualified residence interest” on a loan of up to $1 million secured by a qualified residence, plus interest on a home equity loan up to $100,000.

No comments:

Post a Comment